GFG Resources: Main Takeaways From Call With Management

Company data

- Website: https://www.gfgresources.com/Home/default.aspx

- Stock Ticker: GFG

- Shares Outstanding: 50.3 Million

- Shares Outstanding (fully diluted): 53.0 Million

- Market Cap (fully diluted @ C$0.57): C$30 (US$23 Million)

- Insider Ownership: 14%

- Institutional Investors: Zebra Holdings, US Global, Sentry, Machenzie & AGF.

- Cash: US$4.0 Million (June 30)

My bullet points from the call with CEO Brian Skanderbeg and VP Marc Lepage:

- Next batch of drill results expected very soon. (Hopefully ahead of Zurich which GFG and I will attend)

- News release will contain Brownfield Targets.

- Some Greenfield drilling is complete.

- Looking to raise money in Q4 or Q1 2018.

- The 114m drill intercept in the latest news release hit mostly oxides.

- Finding sub horizontal continuity/connection between zones that was a positive surprise.

- Somewhat adjusting the drill campaign in light of that.

- Looking for additional projects to hopefully enable an even more continuous/steady news flow.

- They understand the market is tough and preserved some cash to prolong the time window for potential funding.

- Cowboy target is looking better than expected.

- Mineralization characteristics are similar to Cripple Creek and the Wharf Mine, with high grade zones and lower grade halos.

Note: I can’t guarantee I interpreted everything 100% correct but those were the notes I wrote down.

Horseman’s comments

Brian mentioned that they knew they could get a “barn burner” news release simply by infill drilling the high grade stuff at North Stock, but chose to spend the money on step out holes and actually create value for shareholders (A sign of true professionals focused on actual value creation in my opinion).

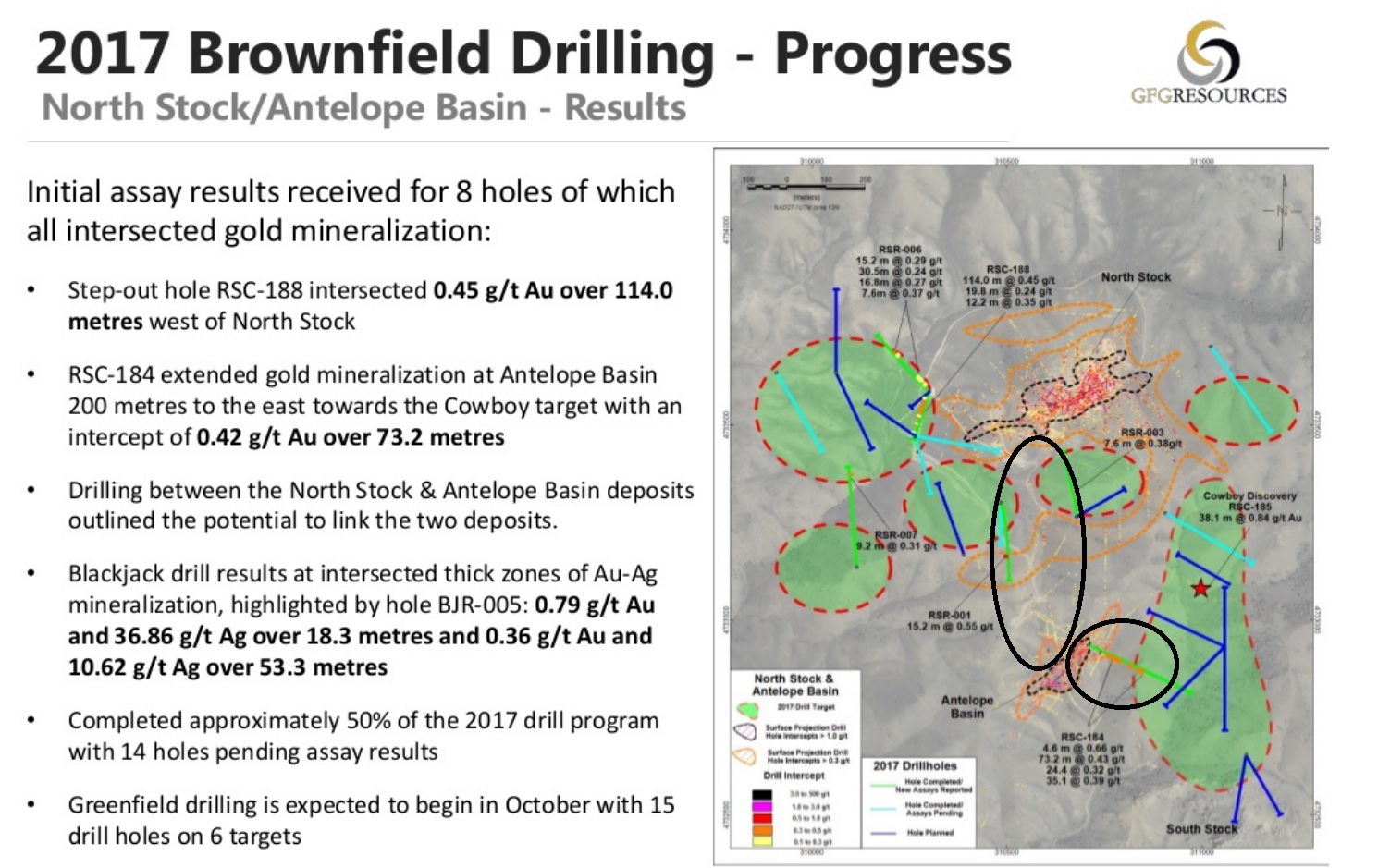

The big thing in terms of the actual deposit was no doubt the signs that the east target might extend (and connect) to the Antelope Basin target. That would mean more tonnage and possibly improved economics. This possible connection is in addition to the potential connection between North Stock and Antelope Basin:

Source: Company presentation.

My personal belief is that the Rattlesnake Hills deposit will get a lot bigger in the future. The previous operators seem to have focused a lot of drill meters on areas where they already know there is gold. What I’m basically saying is that I think the team behind GFG will create more actual value per meter drilled than the former operator Evolving Gold did, which is an important point for shareholders.

The team behind GFG Resources includes both exploration geologists as well as mine builders/operators. They know what mid tier and major producers want… An actual deposit that is both large and most importantly, works. Drilling the same high grade spot and pumping out “barn burners” will perhaps draw the attention of retail investors, but it won’t draw more attention from large producers.

Investors should not be overly focused on the relatively low grade hits from the latest news release. There are plenty of mines that have a resource grade of sub 1 gpt that are still cash cows. Couer Mining’s Wharf Mine would be a perfect example of that, which mines the oxides only. The mining at Cripple Creek on the other hand includes both oxides and sulfides which lowers recovery numbers but takes it back through “economies of scale” (much larger production numbers).

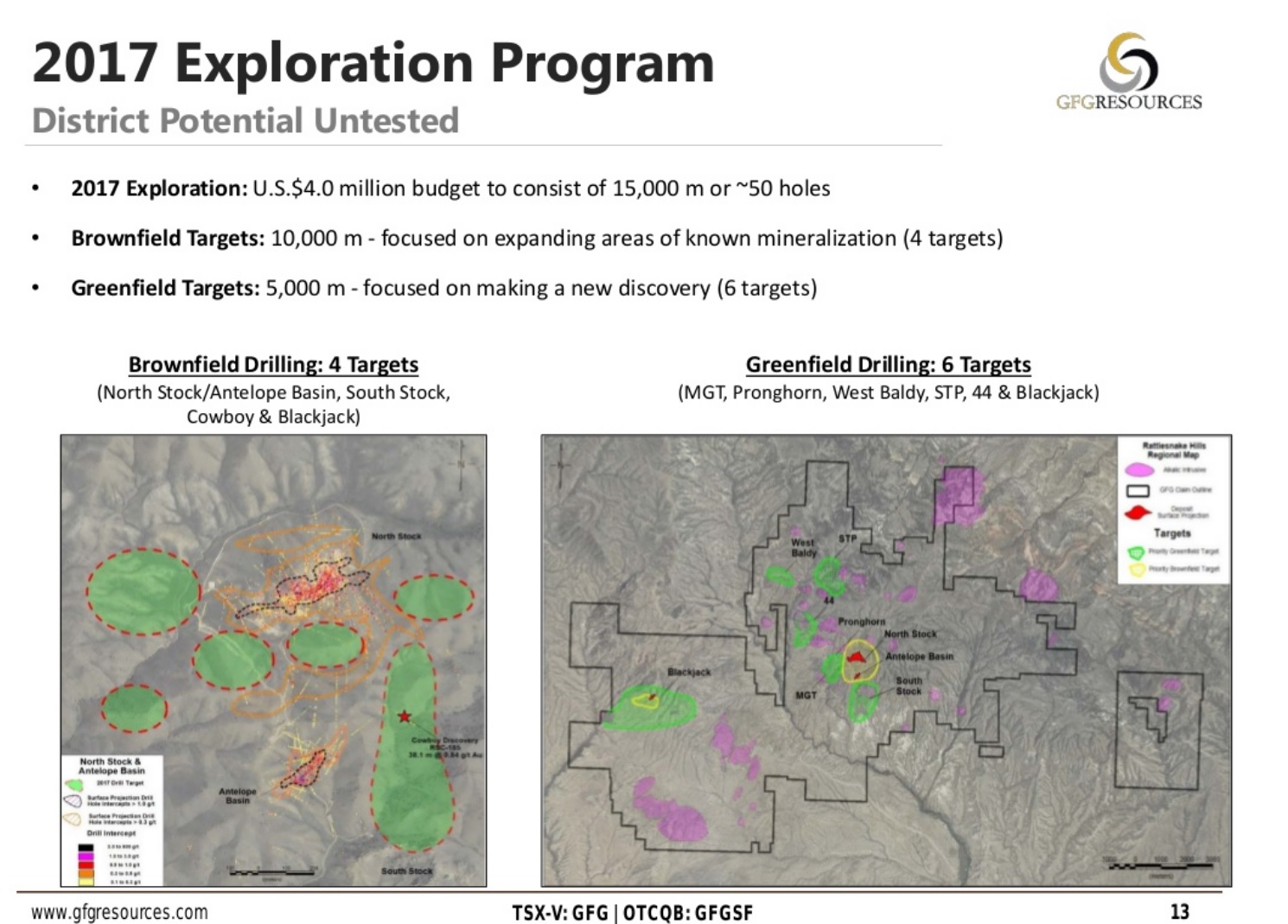

Keep in mind that GFG Resources has district scale potential:

Source: Company presentation.

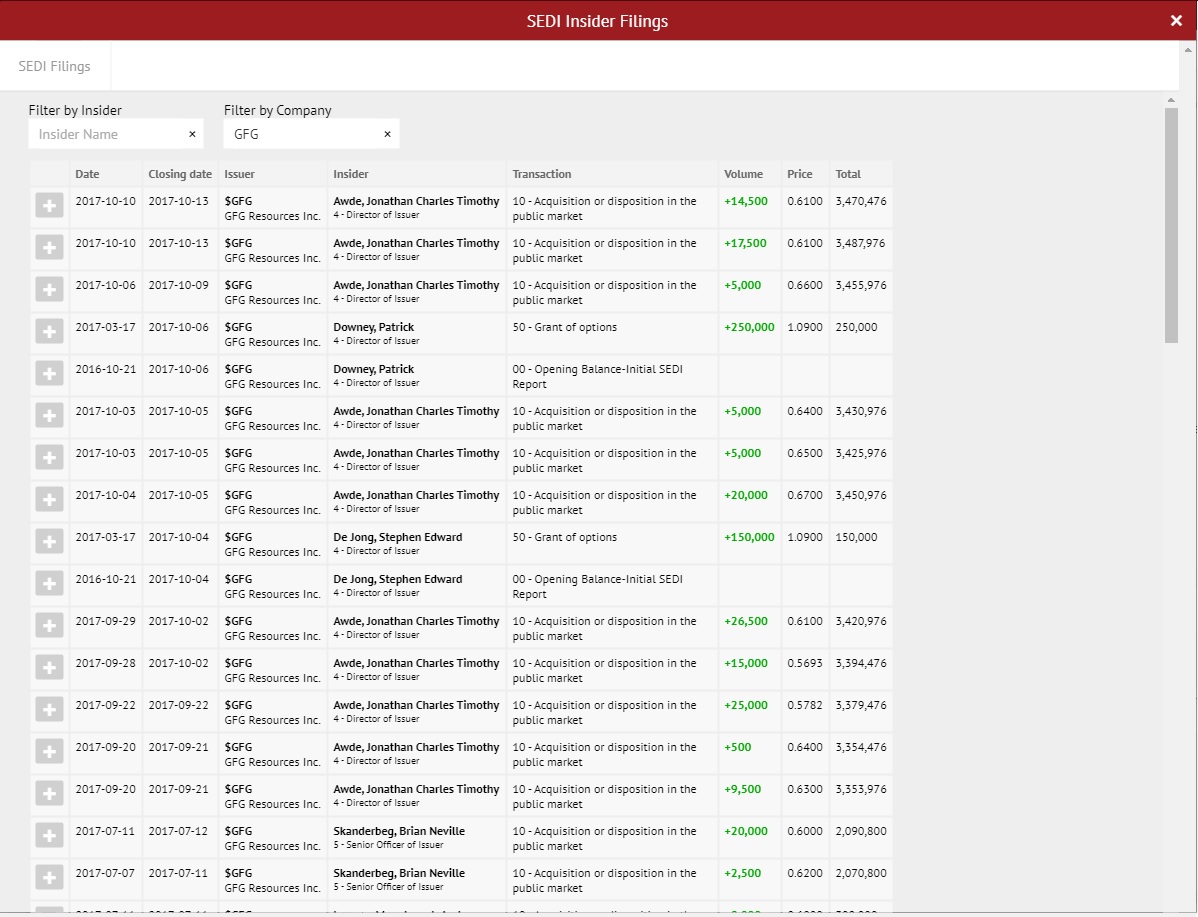

Lastly, let’s look at the latest SEDI Insider Activity:

Insider activity – Source: CEO.ca

… A sea of green. Given how often thinly traded the stock is, investors can’t really ask for a prettier picture than that.

My initial report on GFG Resources can be found HERE.

Disclaimer: This is not a buy or sell recommendation. Everyone is responsible for their own investment decisions. I own stock of GFG Resources and am thus biased. Always do your own due diligence. I have not received any compensation for writing this article. The content in this article was written by me and only me.