Time is Valuable

Time has value.

An ounce in the ground is only valuable if it can be recovered economically.

Thus, time to economic recovery is a big deal…

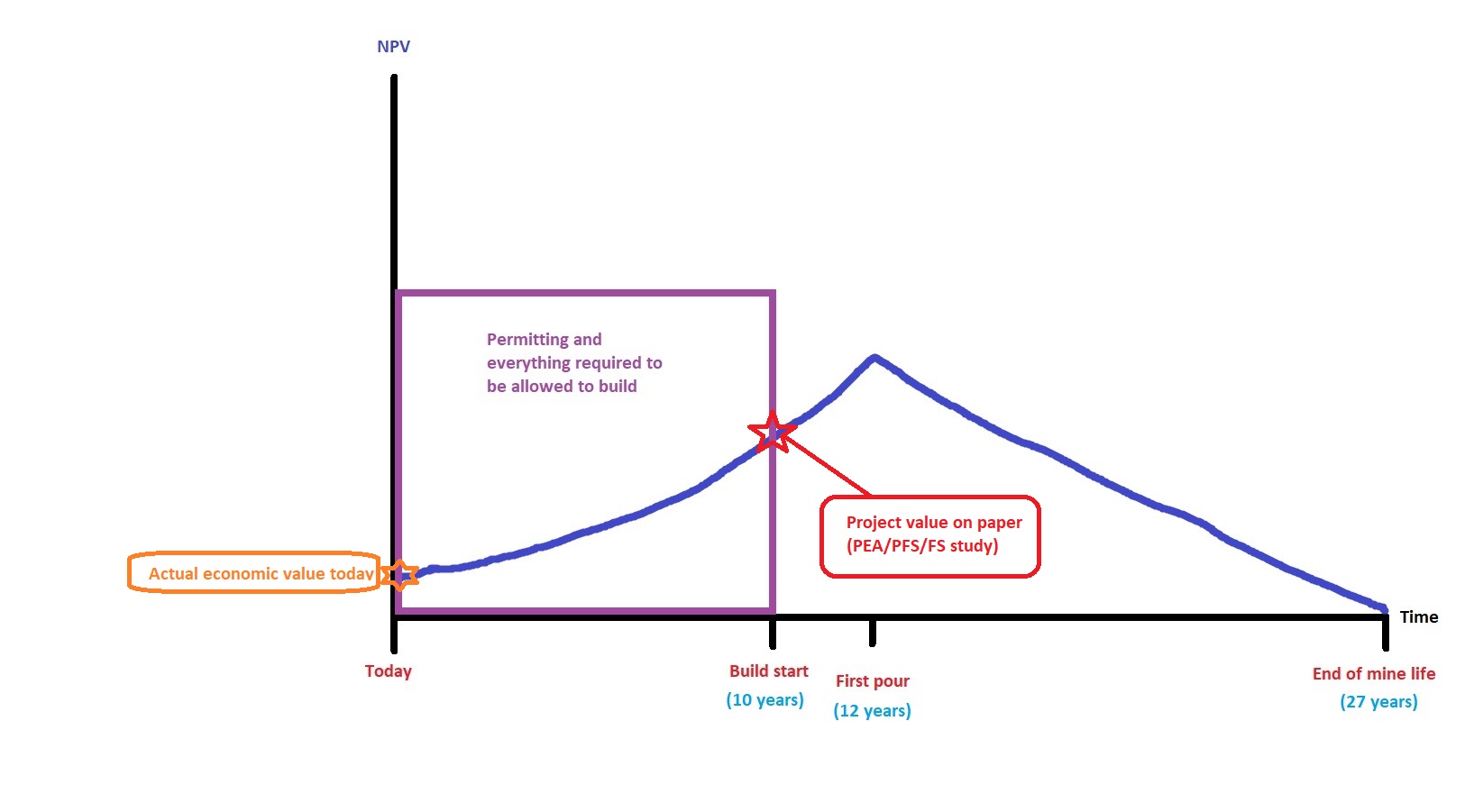

What is the value of a project that is fully permitted, shovel ready and is worth $500 M on paper?

What is the value of a project that is not permitted, shovel ready but is also worth $500 M on paper?

If you have a project that is worth $500 M on paper but will start to be built in ten years then the NPV (today) is only $307 M with a low discount rate of 5%.

If we use a discount rate of 10% then the NPV (today) is instead $192 M.

This means that de-risking efforts such as environmental permits etc are quite valuable because it means that a given income stream is theoretically closer at hand.

A fully permitted project has much less opportunity cost than a project that is 10 years from being fully permitted and shovel ready.

This is something that is seldom discussed because juniors are de facto “trading sardines”.

If a junior finds something that would be worth $1 B in today’s money but will realistically not be fully permitted and shovel ready in 10 years then the NPV today would be $385 M with a 10% discount rate and $614 M with a 5% discount rate.

Two important factors to consider when it comes to what a suitable discount rate would be is that a) The mining business is very risky and b) Rates around the world are at all time lows.

The former suggests one should use a high discount rate while the latter suggests a low to almost non existent discount rate.

… So what is a suitable discount rate? 0%? 5%? 10%? 15%?

I don’t know.

Is this something that a lot of investors have in mind?

I don’t think so.

Are there many investors in this sector?

Honestly, I don’t think so.

This sector is so bad on average that most are forced to become traders.

Imagine what economic damage the major miners do when they buy an advanced exploration or development project at year X…

5 years later it might not be fully permitted and the commodity prices could be in a bear market…

Not only is the NPV for the project much lower but in hind sight that NPV should be discounted by an additional 5 years at least…

Which theoretically can mean that if the acquirer paid full value (full NPV at the then prevailing gold prices) for a project then the value of that asset could be down 70% in five years (during the beat market) and the time value of money dictates that the value in hind sight was the 5 year discounted value of the remaining 30% in NPV.

More time also means means more political risk since the probability of anything happening increases with the time horizon (Same reason why investors demand higher rates from longer maturity bonds)

Conclusions

- De-risking efforts that brings a project closer to being fully permitted and shovel ready actually matters a lot in a rational reality

- Projects that are unlikely to get built, at least anytime soon, are probably overvalued a lot of the time

- Which means jurisdiction etc is more important than many think

- It’s best to stick to tier 1 exploration juniors that actually have a chance to either;

- a) Get bought out by a major and let shareholders get paid up front

- b) Have enough exploration potential that the company could possibly “outrun” the discounting in the case that they add more value than gets eaten up by the value of time.

- Remember to keep in mind that the NPV of a project assumes build start is TODAY

- A junior can add on as many ounces on the books as it wants but if the build start is 10 years out then the NPV for all those ounces TODAY should be discounted by 10 years

- All of the above assumes constant gold prices

- With that said we all see a lot of people include statements like “If gold goes to X,000 then this should fly!”…

- Even though the same could be said for every peer as well

- Ease of permitting and probability of being able to keep the project until the value is realized is important (for an investor at least)

Crude example of the actual NPV of a project that takes 10 years to get fully permitted and shovel ready:

… Remember that the NPV in a PEA/PFS/FS assumes a build start TODAY pretty much

Some examples of the value (cost) of time:

- A project with a NPV of $500 M decreases to $392 M today if it takes 5 years until build start with a 5% discount rate

- A project with a NPV of $500 M decreases to $356 M today if it takes 5 years until build start with a 7% discount rate

- A project with a NPV of $500 M decreases to $310 M today if it takes 5 years until build start with a 10% discount rate

- A project with a NPV of $500 M decreases to $254 M today if it takes 10 years until build start with a 7% discount rate

… After reading this article I hope someone will understand why the thought of there being a lot of “investors” in this space sounds very far fetched to me.

I also think it is ABSOLUTELY critical to understand if you own something that might actually be an investment, which includes a good business model/plan, or if you are holding one of many trading sardines out there.

One ought not to HODL a trading sardine.

Best regards,

Erik Wetterling aka “The Hedgeless Horseman”

Follow me on twitter: https://twitter.com/Comm_Invest

Follow me on CEO.ca: https://ceo.ca/@hhorseman

Follow me on Youtube: My channel

Rick Rule recently said that typical cost of capital for a junior miner is 15%. He was laughing at the typical 5% discount rate used in NPV calculations by juniors.

Hopefully, Novo Resources has already absorbed this cost. Their cash on hand, Sumitomo commitment, and possible cash flow from Beaton’s Creek may be all Novo needs?

While on the topic of Novo–

1. Is it just me, does Novo never talk about selling out to a major? No. Interesting.

2. Note all the Novo land holding on the NW coastline of Australia. Do they suspect the alluvial erosions that start in the Egina area go all the way to the coast? I have never heard any discussion about the coastal holdings in any public domain. Interesting.

3 The JV pioneer in Egina is this… http://www.pioneerresources.com.au/

and here is link to their press release about Novo’s recent Egina news….https://wcsecure.weblink.com.au/pdf/PIO/02253676.pdf

“One ought not to HODL a trading sardine.” Erik, do I detect your entry into the crypto world? Only people involved in the crypto market would understand HODL – the act of buying and holding. One that buys and holds is known as a hodler. Maybe you watched those videos I recommend to you a while back.