Kereport: Novo Update From QH

I thought I would just summarize some things from the Kereport interview with Quinton that was published a few hours ago, as well as make a few comments on Egina which I did not have the time to put into my last article.

- LINK to the interview with Kereport.com

- Full transcript courtesy of JustJT.

Comet Well (West Mt Roe Conglomerates)

- Took samples form both units, as well as a bit above and below each unit

- “We had to … determine the boundaries”

- Some of the samples people see today are taken from barren material.

- Lower Canonball Conglomerate (Gold bearing unit):

- 1.4m of average 6.1 g/t.

- 1.8m of average 2.4 g/t.

- Avg grade 4.25 g/t

- Fine gold content varies from sample to sample.

- “We do think most of the gold is associated with nuggets”

- Upper Cannonball Conglomerate:

- 0.6m of 1.22 g/t

- 0.8m of 2.26 g/t

- 0.4m of 4.53 g/t

- 0.4m of 1.29 g/t

- 0.4 m of 3.06 g/t

- Nuggets tend to be larger.

- They COULD probably get much much higher grades if they wanted to (detect and then sample a high nugget concentration)

- Samples out should be fairly reflective of the overall “background” grade

- The avg grade in the Witwatersrand conglomerates is around 6 g/t.

- If you take an aggregate of the Mt Roe conglomerates of say 2-3m at AVG 2.5 g/t, you get about the same gold inventory as in the Wits.

- Goal is to get data from sampling and diamond drilling to convert the exploration licences to mining leases.

- Then go to trial mining.

Egina

- Already have mining leases.

- “It’s on the same conglomerate system”.

- What they think has happened is that the gold bearing conglomerates have been eroded over time and then the liberated gold has been left in lag gravels, sitting right at surface.

- “If we had known about Egina 18 months ago, we would have probably started there. I’ll be frank. As crazy as it sounds“.

- Will soon come out with plans describing how they will move this new district scale target forward.

- Two targets: Not only do they see the conglomerate potential at Egina, the also see potential in these lag gravels.

- They anticipate it should be a project that is easier to move forward (compared to Comet Well/Purdy’s).

- Should be able to do test work internally within the company rather than going through a long laborious process (SGS).

- The nuggets in the lag gravels (“terrace flats”) look ever coarser than at Karratha. (HH: Closer to the source I wonder…?).

What makes Egina so great is that mother nature has “chopped up” and eroded away the rocks that hosts all the gold layers, and simply left the gold in place. Instead of mining the Upper Cannonball Conglomerate and then removing the say up to 15m of (almost) waste rock to reach the Lower Cannonball Conglomerate, mother nature has already removed the waste rock and liberated the gold in parts of Egina from the hard rock.

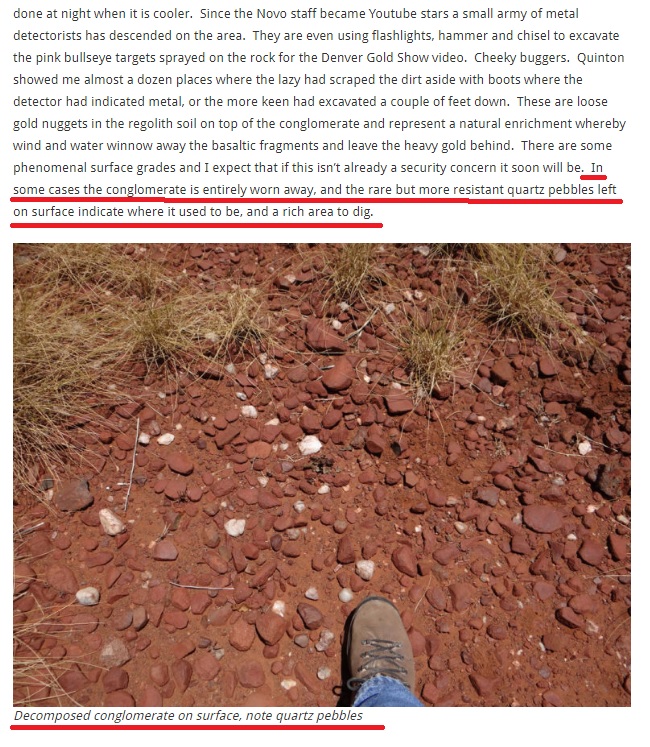

I have posted a lot of pictures with quartz readings for Pilbara since I covered my theories in one of my earlier documents done in 2017, and would like to show you a few slides why at least I considered them to potentially be quite important…

A snippet from Keith Barron’s article that cover Novo and Pilbara:

Source: Straighttalkonmining.com

… NOTE(!): “In some cases the conglomerate is entirely worn away, and the rare but more resistant quartz pebbles left on surface indicate where it used to bem abd a rich area to dig.”

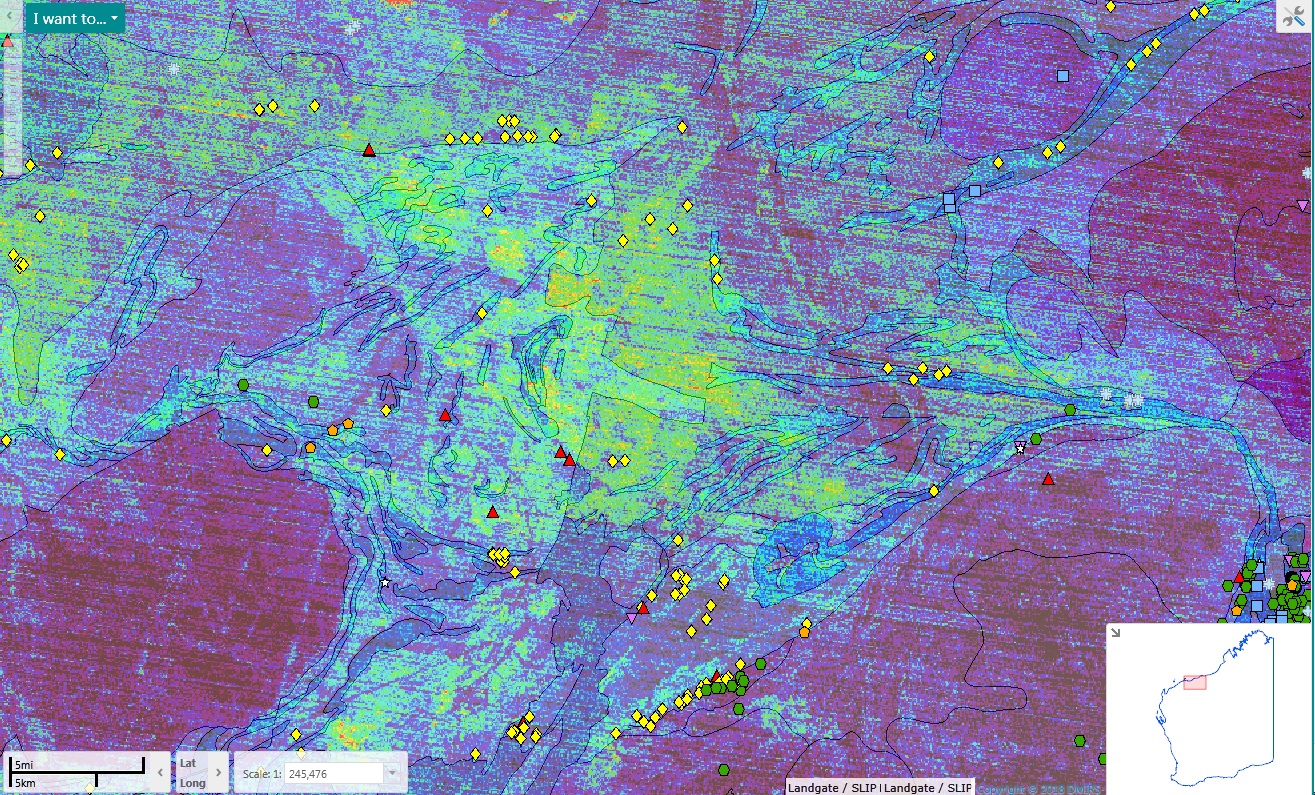

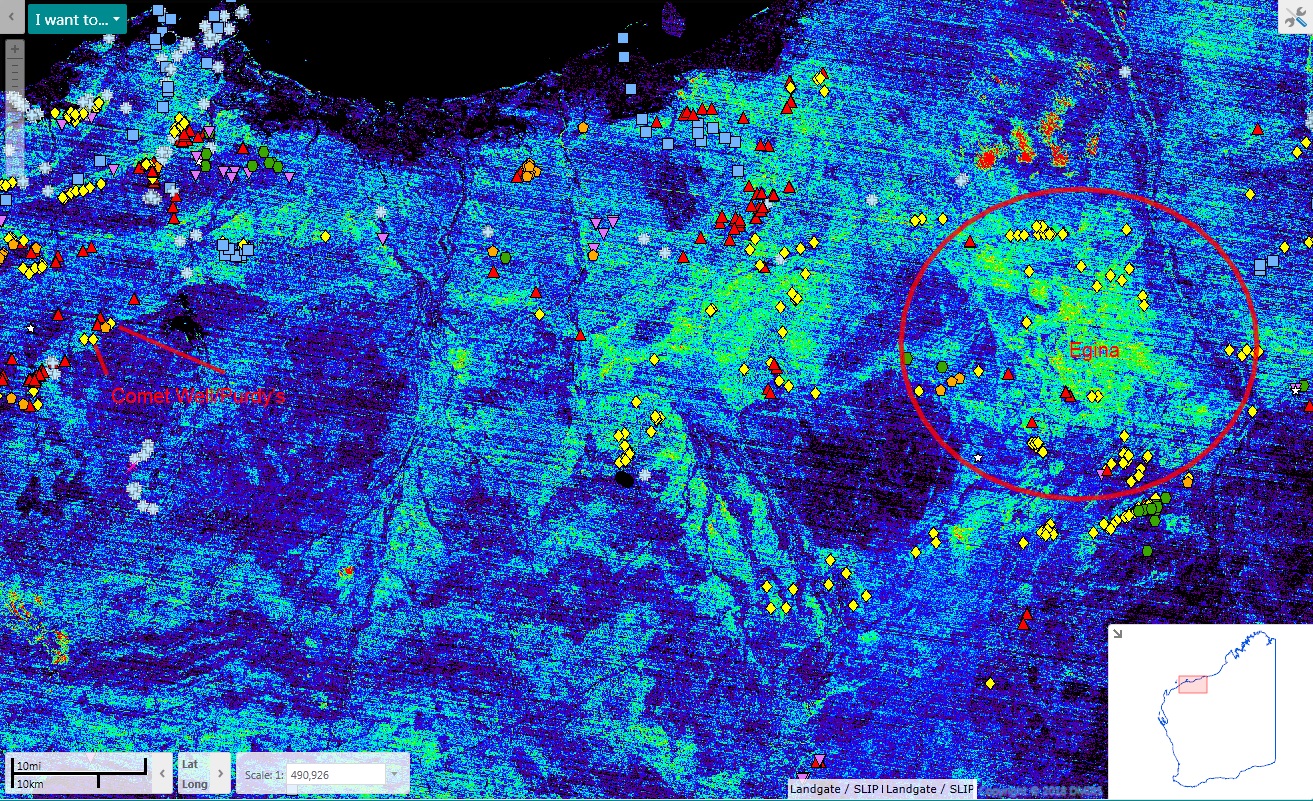

Now lets go back to some of my quartz filter pictures I have been posting for over a year:

- Egina area with a quartz filter:

Egina-Quartz Filter. The Hedgeless Horseman.

… OK, that might not say much to people, but you might get the picture when we compare it to the Karratha area:

Egina-Quartz Filter. The Hedgeless Horseman.

… One can actually spot some “rims” that basically follows the Mt Roe cover near Comet Well and Purdy’s Reward, but the point I am trying to make is that Egina lights up like a Christmas tree compared to most of the Pilbara, where the Mt Roe has already eroded also. Furthermore, one can see that most known gold prospects (in yellow) are concentrated near these high readings. Pilbara is very under-explored, and I think we will uncover a lot in the future… Now you might understand why I have had Novo, Pacton and De Grey in my personal top 4 for quite some time.

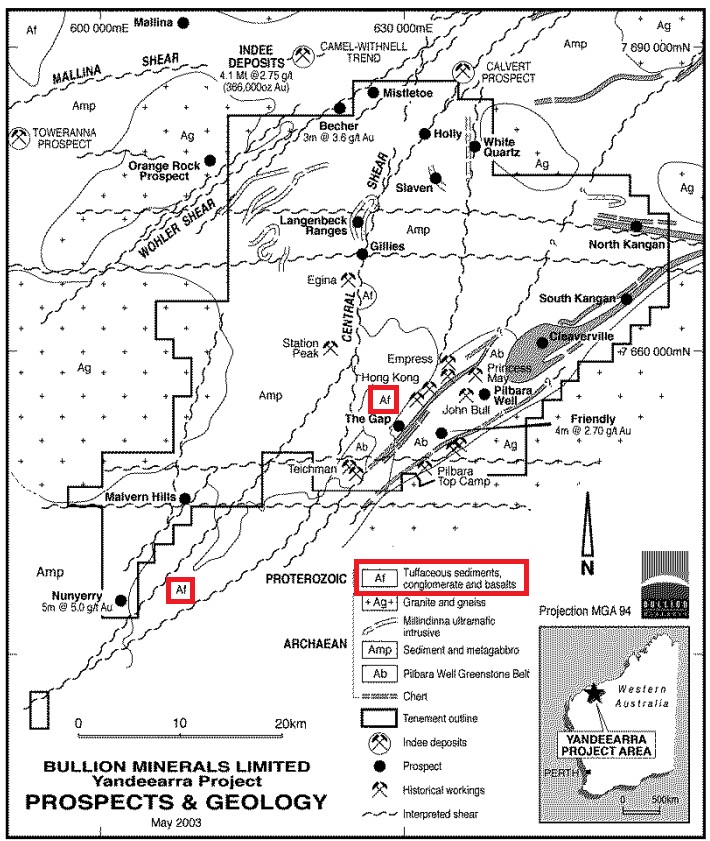

Furthermore, here’s an old geological map for the Egina area:

Kangan/Egina. Source: Bullion Minerals Limited

… Note the “Tuffaceous sedoments, conglomerate and basalts“.

I don’t know how many times I have said I PERSONALLY think that the market is totally clueless and has pretty much ONLY focused on (thus priced in) Comet Well, and that I PERSONALLY think Novo is much much more than just one prospect. Today Quinton said he would probably have started at Egina (“The game changer”) if he knew about it 18 months ago (HH: Man what a pumper I was for pointing out that Novo is much more than CW… And then Quinton basically confirms it a few hours later. Priceless. ). Make of that what you will. I know what I PERSONALLY think Egina type gold might mean for Novo and the Pilbarians, and as always, I think few even account for and/or knows about the new Beaton’s Creek.

But don’t mind me and my clueless “pumping”. There’s obviously a huge amount of people have spent months on DD and knows a lot more than me. Please continue to throw up shares because of some first ever batch of samples that tested a few square meters, at one prospect, from one of the Pilbara targets that Novo controls (Mt Roe). It doesn’t really matter to me, except the fact that I have been able to load up even more shares and lowered by cost basis materially. Novo and the Pilbarians will go where they will go in the long term regardless of what my personal view is. I just happen to think it will be way up over the coming months and years. Only I invest according to my view, and only I will profit (or lose) from it accordingly. Good luck regardless if you sell or buy Novo.

Note! This is NOT investment advice. Junior mining stocks are risky and can be very volatile. Novo Resources has been my largest holding since 2016 and might buy and sell stock at any time. I can’t guarantee 100% accuracy in terms of what is contained in this post and thus would encourage everyone to do their own Due Diligence. This post is contains my personal view on Novo. I have not received any compensation for writing this article.

Best regards,

The Hedgeless Horseman

Follow me on twitter: https://twitter.com/Comm_Invest

Follow me on CEO.ca: https://ceo.ca/@hhorseman

Don’t forget to sign up for my Newsletter (top right on front page) in order to get notification when a new post is up!

If you want to learn more about Novo Resources and the Pilbara Gold Rush you can purchase all my premium content HERE.

If you find my work valuable and want to help me keep publishing most of my research for free then please consider making a donation.

It appears to me from what I’ve read that both Karios and Novo are amazing. Novo has about ten times the value of Karios and Karios is about 1% the cost of Novo which has 10 times the cash of Karios. Both have excellent value. Novo leadership has a better understanding of what they have which makes them less likely of being ripped off, but Karios is using Novos’ original exploration expert, which could educate them real quick. We are talking about over 10 billion ounces in the system which keeps the critics bad mouthing as impossible. Maybe the critics are right, but the field is in the right place to be one of the greatest fields of all times. I’m poor, with no boots on the ground, but have invested what I can. I’m no expert nor probably ever will be. I may someday be rich if God wills. I am a believer who thinks just maybe the assays and sampling procedures aren’t lying and the dried up ocean (large lake) with a two-meter layer of gold deposit is real. I am also a well-trained scientist who recognizes good, scientific process when I read about it. I hope this is real and the corporate leaders are wise, carrying about their stockholders. God bless….use your own due diligence

As soon as/if proof of concept is confirmed from either of the basin scale targets, I am sure all Pilbara juniors with a chunk of good land will do great.

Honestly, I don’t think the critics can use a calculator. It’s not that us bulls are 100% it’s a “new Wits”, it’s that nothing of the sort is priced in and I do believe the market has given us very favorable odds since I do believe there is more than say a 5% chance of them unlocking _something_, and better than say a 1% chance that they actually are onto something of outrageous size. If Kirkland said Novo for example was at least worth $5 just a couple of months ago, then I’m not that worried buying Novo and the Pilbarians for 50%+ off.

Best regards,

HH